Crisis revisited

The euro is still vulnerable, and Greece is not the only problem

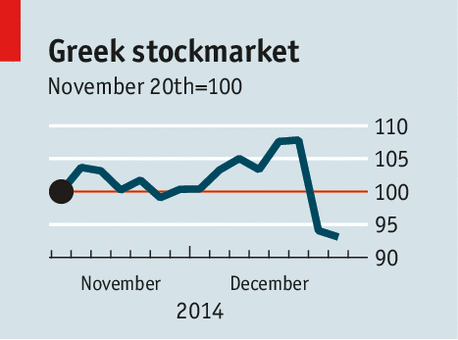

The proximate cause of the latest outbreak of nerves was the decision by the Greek government, now headed by the generally competent Antonis Samaras, to advance the presidential election to later this month. The presidency is largely ceremonial, but if Mr Samaras cannot win enough votes in parliament for his candidate, Stavros Dimas, a general election will follow. Polls suggest the winner would be Syriza, a populist party led by Alexis Tsipras. Although Mr Tsipras professes that he does not want to leave the euro, he is making promises to voters on public spending and taxes that may make it hard for Greece to stay. Hence the markets’ sudden pessimism.

As it happens, there is a good chance that Mr Dimas, a former EU commissioner, will win the presidential vote at the end of this month (see article). But the latest Aegean tragicomedy is a timely reminder both of how unreformed the euro zone still is and of the dangers lurking in its politics.

It is true that, ever since the pledge by the European Central Bank’s president, Mario Draghi in July 2012 to “do whatever it takes” to save the euro, fears that the single currency might break up have dissipated. Much has been done to repair the euro’s architecture, ranging from the establishment of a bail-out fund to the start of a banking union. And economic growth across the euro zone is slowly returning, however anaemically, even to Greece and other bailed-out countries.

But is that good enough? Even if the immediate threat of break-up has receded, the longer-term threat to the single currency has, if anything, increased. The euro zone seems to be trapped in a cycle of slow growth, high unemployment and dangerously low inflation. Mr Draghi would like to respond to this with full-blown quantitative easing, but he is running into fierce opposition from German and other like-minded ECB council members (see article). Fiscal expansion is similarly blocked by Germany’s unyielding insistence on strict budgetary discipline. And forcing structural reforms through the two sickliest core euro countries, Italy and France, remains an agonisingly slow business.

Advertisement

Japan is reckoned to have had two “lost decades”; but in the

past 20 years it grew by almost 0.9% a year. The euro zone, whose

economy has not grown since the crisis, is showing no sign of dragging

itself out of its slump. And Japan’s political set-up is far more

manageable than Europe’s. It is a single political entity with a

cohesive society; the euro zone consists of 18 separate countries, each

with a different political landscape. It is hard to imagine it living

through a decade even more dismal than Japan’s without some political

upheaval.Greece is hardly alone in having angry voters. Portugal and Spain both have elections next year, in which parties that are fiercely against excessive austerity are likely to do well. In Italy three of the four biggest parties, Forza Italia, the Northern League and Beppe Grillo’s Five Star movement, are turning against euro membership. France’s anti-European National Front continues to climb in the opinion polls. Even Germany has a rising populist party that is against the euro.

It’s the politics, stupid

Indeed, the political risks to the euro may be greater now

than they were at the height of the euro crisis in 2011-12. What was

striking then was that large majorities of ordinary voters preferred to

stick with the single currency despite the austerity imposed by the

conditions of their bail-outs, because they feared that any alternative

would be even more painful. Now that the economies of Europe seem a

little more stable, the risks of walking away from the single currency

may also seem smaller.Alexis de Tocqueville once observed that the most dangerous moment for a bad government was when it began to reform. Unless it can find some way to boost growth soon, the euro zone could yet bear out his dictum.

No comments:

Post a Comment